The general economics or viability of a refinery is determined by the interplay of three key elements: the choice of crude oil used (crude slates), the complexity of the refining gear (refinery configuration) and the desired type and high quality of products produced (product slate). Refinery utilization rates and environmental considerations also influence refinery economics.

Using dearer crude oil (lighter, sweeter) requires less refinery upgrading however provides of mild, sweet crude oil are lowering and the differential between heavier and more sour crudes is growing. Using cheaper heavier crude oil means extra funding in upgrading processes. Prices and payback intervals for refinery processing units should be weighed towards anticipated crude oil prices and the projected differential between mild and heavy crude oil prices.

Using dearer crude oil (lighter, sweeter) requires less refinery upgrading however provides of mild, sweet crude oil are lowering and the differential between heavier and more sour crudes is growing. Using cheaper heavier crude oil means extra funding in upgrading processes. Prices and payback intervals for refinery processing units should be weighed towards anticipated crude oil prices and the projected differential between mild and heavy crude oil prices.

Crude Oil Enter

Crude oil is the primary enter into the petroleum refining industry. While Canada is a big and rising web oil exporter, crude oil imports fulfill greater than half of domestic refinery demand. The transportation prices related to transferring crude oil from the oil fields in Western Canada to the consuming regions within the east and the better choice of crude qualities make it extra financial for some refineries to make use of imported crude oil. Therefore, Canada’s oil economic system is now a dual market. Refineries in Western Canada run domestically produced crude oil, refineries in Quebec and the eastern provinces run primarily imported crude oil, while refineries in Ontario run a mixture of both imported and domestically produced crude oil. In more moderen years, japanese refineries have begun operating Canadian crude from east coast offshore manufacturing.

Whatever the source of crude oil, the value is set on the planet market and each imported and domestic crude oil is priced in response to the availability/demand stability and pricing dynamics on the world oil market. On this respect, Canadian refiners are rice takersand have very little influence on the price they pay for crude oil. Using more expensive crude oil (lighter, sweeter) requires less refinery upgrading but supplies of mild, candy crude oil are reducing and the differential between heavier and extra bitter crudes is growing. Using cheaper heavier crude oil means more investment in upgrading processes. Prices and payback intervals for refinery processing items should be weighed in opposition to anticipated crude oil prices and the projected differential between light and heavy crude oil costs.

Crude slates and refinery configurations must take into consideration the type of products that will finally be needed within the marketplace. The standard specifications of the final merchandise are additionally more and more necessary as environmental necessities grow to be more stringent.

Crude Slates

Several types of crude oil yield a different mix of merchandise depending on the crude oil’s natural qualities. Crude oil sorts are typically differentiated by their density (measured as API gravity) and their sulphur content material. Crude oil with a low API gravity is taken into account a heavy crude oil and typically has a higher sulphur content material and a bigger yield of decrease-valued merchandise. Subsequently, the lower the API of a crude oil, the lower the worth it has to a refiner as it can both require extra processing or yield a higher share of lower-valued by-merchandise resembling heavy fuel oil, which normally sells for lower than crude oil.

Crude oil with a high sulphur content material known as a bitter crude whereas sweet crude has a low sulphur content material. Sulphur is an undesirable characteristic of petroleum products, significantly in transportation fuels. It may well hinder the environment friendly operation of some emission control applied sciences and, when burned in a combustion engine, is launched into the atmosphere where it may possibly form sulphur dioxide. With more and more restrictive sulphur limits on transportation fuels, candy crude oil sells at a premium. Bitter crude oil requires more severe processing to take away the sulphur. Refiners are typically prepared to pay more for light, low sulphur crude oil.

Most refineries in Western Canada and Ontario were designed to course of the sunshine candy crude oil that’s produced in Western Canada. In contrast to leading refineries in the U.S., Canadian refineries in these regions have been slower to reconfigure their operations to process lower price, less fascinating crude oils, instead selecting to rely extensively on the abundant, domestically produced, mild, candy crudes. So long as these lighter crudes had been out there, refining economics were insufficient to warrant new investment in heavy oil conversion capacity.

Nonetheless, with growing oil sands manufacturing and the declining production of typical mild sweet crudes, refineries in Western Canada and Ontario have started to make the investment required to process the increasing provide of heavier crudes. A lot of this investment by the large integrated oil firms (corporations which might be involved in both the production of crude oil and the manufacturing and distribution of petroleum products) is associated with ensuring a market for his or her rising oil sands production.

In Western Canada and Ontario, virtually 50% of the crude oil processed by refiners is typical light, sweet crude oil and one other 25% is top quality synthetic crude oil. Synthetic crude is a gentle crude oil that is derived by upgrading oil sands. Many of the remaining crude oil processed by these refineries is heavy, bitter crude. The crude slate is anticipated to alter considerably in the years forward as refiners improve their capacity to process heavy crude oil and decrease quality artificial crudes.

Refineries in Atlantic Canada and Quebec are dependent on imported crudes and tend to course of a extra various crude slate than their counterparts in Western Canada and Ontario. These refiners have the capacity to buy crude oil produced almost anyplace on the planet and therefore have unimaginable flexibility of their crude shopping for choices. Approximately 1/three of crude processed in Eastern Canada and Quebec is conventional, mild candy crude and one other 1/three is medium sulphur, heavy crude oil. The remaining 1/3 is a mix of sour gentle, bitter heavy and very heavy crude oil. The crude slate in Eastern Canada is anticipated to stay rather more static than that in Western Canada and Ontario, as these refiners are not constrained by the standard or quantity of home crude production.

Refinery Configuration

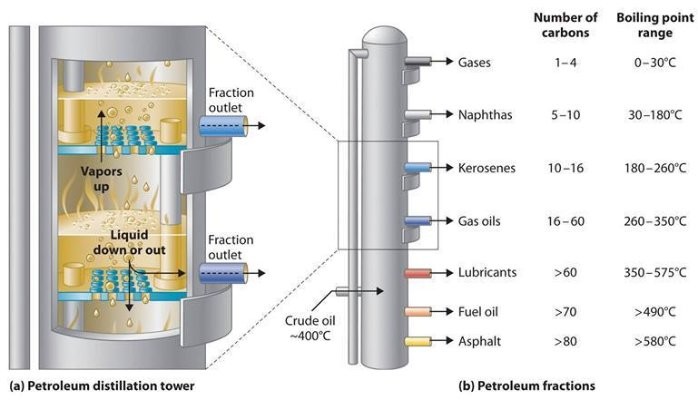

A refiner’s alternative of crude oil shall be influenced by the kind of processing items at the refinery. Refineries fall into three broad categories. The only is a topping plant, which consists only of a distillation unit and possibly a catalytic reformer to supply octane. Yields from this plant would most intently mirror the natural yields from the crude processed. Usually solely condensates or gentle candy crude would be processed at this kind of facility unless markets for heavy fuel oil (HFO) are readily and economically accessible. Asphalt plants are topping refineries that run heavy crude oil as a result of they are solely excited by producing asphalt.

The next stage of refining is known as a cracking refinery. This refinery takes the gas oil portion from the crude distillation unit (a stream heavier than diesel fuel, but lighter than HFO) and breaks it down further into gasoline and distillate elements utilizing catalysts, high temperature and/or strain.

The last degree of refining is the coking refinery. This refinery processes residual gasoline, the heaviest materials from the crude unit and thermally cracks it into lighter product in a coker or a hydrocraker. The addition of a fluid catalytic cracking unit (FCCU) or a hydro cracker significantly increases the yield of upper-valued merchandise like gasoline and diesel oil from a barrel of crude, allowing a refinery to process cheaper, heavier crude while producing an equivalent or larger volume of high-valued products.

Hydrotreating is a process used to take away sulphur from completed merchandise. Because the requirement to produce extremely low sulphur merchandise will increase, additional hydrotreating capability is being added to refineries. Refineries that at the moment have giant hydrotreating capability have the flexibility to process crude oil with the next sulphur content.

Canada has primarily cracking refineries. These refineries run a mix of gentle and heavy crude oils to fulfill the product slate required by Canadian shoppers. Historically, the abundance of domestically produced gentle sweet crude oils and a higher demand for distillate products, akin to heating oil, than in some jurisdictions decreased the necessity for upgrading capacity in Canada. Nevertheless, in more recent years, the availability of mild candy crude has declined and newer sources of crude oil tend to be heavier. Lots of the Canadian refineries are actually being equipped with upgraders to handle the heavier grades of crude oil at present being produced.

Product Slates

Refinery configuration is also influenced by the product demand in each area. Refineries produce a wide range of merchandise including: propane, butane, petrochemical feedstock, gasolines (naphtha specialties, aviation gasoline, motor gasoline), distillates (jet fuels, diesel, stove oil, kerosene, furnace oil), heavy gasoline oil, lubricating oils, waxes, asphalt and nonetheless fuel. Nationally, gasoline accounts for about forty% of demand with distillate fuels representing about one third of product sales and heavy fuel oil accounting for only eight % of gross sales.

Whole petroleum product demand is distributed almost equally throughout the areas, with Atlantic/Quebec, Ontario and the West every accounting for about one third of total gross sales. Nevertheless, the mix of products varies quite considerably among the areas.

In the Atlantic provinces, where furnace oil (mild heating oil) is the first source of dwelling heating, distillate fuels make up forty% of product demand, and heavy gasoline oil, used to generate electricity, accounts for one more 24%. Gasoline sales account for lower than 30% of product demand.

In Quebec, the place natural fuel and hydroelectricity are prevalent, distillate gasoline has a 34% share of sales and gasoline is about forty%. Similarly, in Ontario, gasoline sales outpace distillate sales and account for greater than forty five% of whole product demand, with distillates at less than 30%.

In Western Canada, agricultural use is one of the primary drivers behind distillate demand and gasoline and distillate every account for about forty% of complete petroleum product sales. These regional variations in product demand have influenced the configurations of the refineries in each space.

By comparison, within the U.S., the demand for gasoline is much larger than distillate demand and, due to this fact, refiners configure their installations to maximise gasoline production. Gasoline gross sales account for almost 50% of demand whereas distillate gross sales account for lower than 30% of product demand. In several Western European countries, most notably Germany and France, insurance policies exist that encourage using diesel engines creating a a lot stronger distillate element. Gasoline accounts for lower than 20% of petroleum product gross sales in Europe.

The US refineries are configured to process a large proportion of heavy, high sulphur crude and to supply massive portions of gasoline, and low quantities of heavy gasoline oil. U.S. refiners have invested in more complicated refinery configurations, which permit them to use cheaper feedstock and have a higher processing functionality.

Canada’s refineries should not have the high conversion functionality of the US refineries, as a result of, on common, they course of a lighter, sweeter crude slate. Canadian refineries additionally face a better distillate demand, as a percent of crude, than those found within the U.S. so gasoline yields aren’t as high as those in the US, but are still considerably increased than European yields.

The relationship between gasoline and distillate sales can also create challenges for refiners. A refinery has a restricted vary of flexibility in setting the gasoline to distillate production ratio. Beyond a sure level, distillate manufacturing can solely be elevated by additionally growing gasoline production. Because of this, Europe is a major gasoline exporter, primarily to the U.S.

Refinery Utilization

One other critical part of refining economics is the utilization price, or how efficiently the refining advanced is operating. The Canadian refining sector has undergone vital rationalization in the last three decades. In the early 1970s, there have been 40 refineries in Canada. Since that point a number of components have contributed to a significant rationalization of firm operations. The oil price shocks in 1973 and 1979 led to improvements in the effectivity of autos and to fuel switching from oil to natural gasoline and electricity. This curbed the demand for petroleum products and resulted in a substantial surplus of refining capacity. The spare capacity resulted in elevated competition among refiners, which further eroded refining margins. Less efficient, smaller refiners have been closed, generally in favor of recent bigger facilities.

Weak financial situations in the early 1980s put additional stress on the trade to rationalize their operations, resulting in a big number of refinery closures. At this time there are 19 refineries producing petroleum products in Canada. Nonetheless, as a result of expansions on the remaining refineries during the last decade, present refining capacity in Canada is greater than it was within the 1970s.

In recent times, development in the demand for petroleum products has led to an enchancment in capacity utilization, rising operating efficiency and decreasing costs per unit of output. In consequence, refinery utilization rates have been above 90% nationally for six of the last ten years. A utilization price of about ninety five% is considered optimum as it allows for regular shut downs required for maintenance and seasonal changes.

Refinery capability is based on the designed dimension of the crude distillation unit(s) of a refinery (also known as nameplate capability). Sometimes, by means of upgrades or de-bottlenecking procedures, refineries can process extra crude than the nameplate size of the distillation unit would indicate. In such cases, a refinery is ready to attain a utilization rate larger than 100 percent for short intervals of time.

Environmental Initiatives

Not all funding decisions are pushed by refinery economics. Refiners additionally make investment choices because of voluntary actions or legislative and regulatory necessities. In recent times, governments and trade have directed considerable effort towards reducing the environmental influence of burning fossil fuels. Lots of the initiatives have been geared toward providing leaner麓 fuels for Canadians. Petroleum refining is a very sophisticated and capital-intensive industry. New environmental laws require industry to make further investments to satisfy the more stringent requirements.